“Almost no one wants to admit the genius of Jeff Bezos and Amazon. Apparently, many have failed to see that Amazon has become the world's biggest retail company.” Hubert Burda

Consumer spending makes up around 68 percent of the nation’s gross domestic product. Consumer spending is individuals and families purchasing groceries, clothing, recreation, stocks, insurance, education and much more. The transactions cover a broad swath of economic activity.

Much of the nation’s consumer spending is captured via retail trade. A useful retail trade definition is “the re-sale (sale without transformation) of new and used goods to the general public, for personal or household consumption or utilization.” Not all consumer spending is captured through retail trade transactions, but a large share is.

Broad-category examples of retail trade sectors are motor vehicle sales, furniture stores, electronic stores, building material stores, grocery stores, pharmacies, gas stations, clothing stores and department stores, among others.

Then there is the relatively new and emerging part of the retail trade sphere — non-store retailers. These are establishments that sell products on the internet. Examples include Amazon, Zappos, Overstock.com, or eBay. These types of retailers have grown rapidly in the past 15 years and their presence is reshaping the retail trade landscape.

Whereas in the past nearly all retail transactions were done through traditional brick-and-mortar stores, now a significant and growing segment is diverted to internet sales. The consumer shops online and goods are delivered to the customer’s doorstep. One can see that the number of brick-and-mortar stores and the level of local sales across the country are being endangered by this economic evolution.

The brick-and-mortar reduction is beginning to show its economic presence in the United States employment numbers. While the U.S. economy is finally expanding at a healthy pace this side of the Great Recession, one of the few industries not rising with this tide is retail trade. While overall retail sales are increasing, employment is not.

Traditionally, as a population increases, retail trade employment grows simultaneously, since population growth and consumer spending volume is an integrated dynamic. If studied deeply, a certain ratio of retail trade employment growth spawned from population growth would emerge. Before the internet, the vast majority of all consumer sales occurred in the immediate community or region. But now, the internet is diverting these sales away from the local community — and with internet sales growing, its market share will increase.

We do not yet know how much brick-and-mortar erosion will eventually occur. And will such a phenomenon hit some areas more than others (e.g., urban vs. rural, or local vs. tourist spending)? These are touch points that economist will be watching as this Internet sales phenomenon continues to grow within the national and Utah economies.

In light of this change, in this quarter’s Local Insights we are profiling retail trade employment throughout Utah’s local regions. This can offer a profile of where retail trade is now in a local economy, and possibly how much of the sector could become vulnerable to the internet-sales phenomenon.

All regions can be viewed through the Local Insights web portal. The following is a retail trade profile for the Southwest region:

Trending Upward

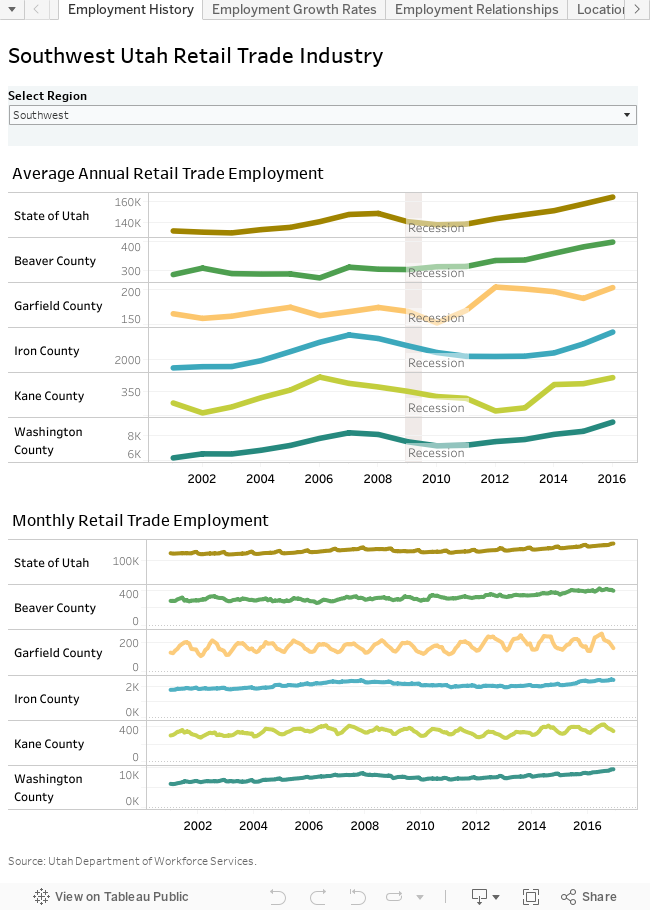

Just how important is retail trade employment in the southwest corner of Utah? In 2016, roughly 12,400 Southwest Utah workers were employed in retail trade representing 14 percent of total nonfarm employment in the region. That’s slightly higher than the statewide retail average of 12 percent. The current employment level represents a regional high point. Moreover, despite the revolution in online buying, employment in retail trade has trended upward in Southwest Utah — although it has ebbed and flowed during boom, recession and recovery. Of course, the region’s population growth provides a major factor in retail trade employment expansion in Southwest Utah.

In most Southwest Utah counties, growth rates swelled in the mid-2000s, toppled during the recession and surged back as the recovery took hold. Yes, retail trade is certainly susceptible to the business cycle. During the recovery, Garfield County led the pack with early retail trade gains only to experience job losses when other counties picked up speed. In contrast, both Kane and Iron counties were slow to add retail jobs in the recovery period. Retail trade employment in both counties just barely returned to the pre-recession peak levels.

Tis the Season

Retail trade employment can be very seasonal in nature. In both the Garfield and Kane economies, a strong tourism and recreation component produces a significant seasonal pattern with employment peaking in the summer months and bottoming out in January or February. In Garfield County, retail trade jobs can double between trough and peak. While tourism isn’t as profound in Beaver County, retail employment also peaks in summer as the industry services travelers along the I-15 corridor. Washington and Iron counties experience less seasonality, but also see their lowest retail employment levels as the year begins. However, in these two counties, holiday shopping creates a slight seasonal peak in December. This pattern follows the statewide lead.

Dependency

Some counties in Southwest Utah are more dependent on retail trade employment than others. Statewide, retail trade employment accounts for about 12 percent of total nonfarm jobs. Beaver (17 percent), Washington (15 percent) and Iron (14 percent) counties all show higher percentages of retail trade employment than the state. Iron and Washington are self-contained, regional shopping centers which probably accounts for their higher-than-average retail shares.

Despite their tourism-dependent economies, Kane and Garfield counties show smaller percentages of retail trade employment overall. This is partially due to the high levels of leisure/hospitality employment in these counties. In addition, tourism’s contribution to retail trade employment typically lasts only half the year.

Location quotients (LQ) provide a different way of looking at the importance of an industry. These ratios compare an area’s industry employment share to that of the nation. A retail trade LQ of 1 indicates the area’s industry employment makes up the same share of employment as that industry does nationwide. A location quotient greater than 1 means the area’s industry has a greater employment share than the United States. Utah’s retail trade location quotient measures just higher than 1. However, Beaver, Iron and Washington counties all have retail trade location quotients of 1.3 or higher, attesting to the magnitude of retail employment in these areas. On the other hand, Kane’s LQ is exactly 1 while Garfield County shows an LQ of 0.78. In other words, retail employment is far less important in Garfield County than in other Southwest Utah counties, the state and the nation.

Over time, the share of retail trade employment has remained fairly steady in the most populated Southwest counties. On the other hand, in Beaver and Garfield counties, retail trade has taken on a more important employment role in the post-recession years.

Relationships

Population per retail worker also provides insights into the retail trade industry’s local importance. Statewide there are roughly 16 residents per retail trade job. Despite being the most tourism-dependent county in Utah, Garfield County shows 24 residents per retail trade worker, the highest in the region. On the other hand, Washington County’s population per retail trade job measures less than 15, which seems to reflect its importance as a regional shopping destination. In general, the ratio of population to retail trade employment has trended downward, which seems to reflect the incursion of online shopping.

Down to Subsectors

In Southwest Utah, general merchandise stores (e.g., Wal-Mart, Target, Dillards, JC Penny) account for the largest subsector share of retail trade workers — 20 percent. Food and beverage stores ran neck-and-neck with these stores with just less than 19 percent of total employment. Motor vehicle/parts dealers (13 percent), building materials/garden stores (12 percent) and gasoline stations (10 percent) are also major employment players in retail trade.

The job shares of retail trade subsectors vary between Southwest Utah and the state overall. Southwest Utah shows higher employment shares in building material and garden stores, food and beverage stores and gasoline stations than Utah. In contrast, the region shows smaller employment percentages in clothing stores, electronics stores and especially non-store retailers. In other words, Southwest Utah employment does not appear to be benefitting from online sales.

A Fair Share?

Since 2000, general merchandise stores have slowly eked out a higher share of retail trade employment. In 2000, roughly 16 percent of Southwest Utah retail employment was at general merchandise stores. Since that time, general merchandise stores have increased their share by 3 percentage points. Building material and garden stores have also seen employment shares increase as several big box retailers entered the area.

On the other hand, food and beverage stores’ share of retail trade employment has decreased slightly. The inclusion of groceries at some big-box stores has probably tapped into some of the food and beverage store employment. On the other hand, many traditional grocery stores now also carry non-grocery items.

Wages

Retail trade is not known for its excessive wages. In 2016, only private education services, and leisure/hospitality services showed lower average monthly wages in Southwest Utah. Not only are retail trade hourly wages lower than average — many jobs are part-time, which contributes to its lower-than-average standing.

Statewide, the average monthly wage for a retail trade worker measures less than $2,600. Not surprisingly, the average retail trade wage measured even lower in all Southwest Utah counties. Nevertheless, a wide disparity in wages exists even within the region. In Washington County, the 2016 average monthly retail trade wage registered at about $2,200, while in Garfield County, the average was a mere $1,400. Iron County’s wage ($2,100) measured slightly below the Washington figure. Beaver ($1,600) and Kane ($1,600) landed closer to the Garfield County wage.

Interestingly, during the pre-recession years when Washington County experienced rapid employment growth and short-term labor shortages, its average monthly retail wage actually surpassed the statewide figure. (It was that whole supply and demand thing at work.) Of course, once recession hit, wages returned to a more historical relationship.

The Same, but Different

Retail trade wages also show a notable variety in relationship to the average county wage. Statewide the retail trade industry wage measures 70 percent of average. In both Iron (84 percent) and Washington (80 percent) counties, retail trade wages compare more favorably to the overall county average. In Beaver and Garfield counties the retail wage measures about 56 percent of average; Kane County’s figure is slightly higher at about 65 percent.

Between 2001 and 2016, the gap between the retail trade industry wage and the average wage widened in all counties — and the state. This suggests that wages in other industries have increased faster than those in retail trade.

Within the retail trade industry in Southwest Utah, jobs at motor vehicle/parts dealers show the highest average wage followed by building materials and garden stores. On the low end of the scale, clothing stores paid the lowest wages.